Understanding of risks, returns and capital deployed is very essential for the Banking, Financial Services and Insurance (BFSI) sector. Keeping this significance in mind, Surya was founded, says D N Prahlad, Founder and Non-Executive Chairman, Surya Software in an interview with Elets News Network (ENN).

Give us an overview of your products and services in the BFSI segment.

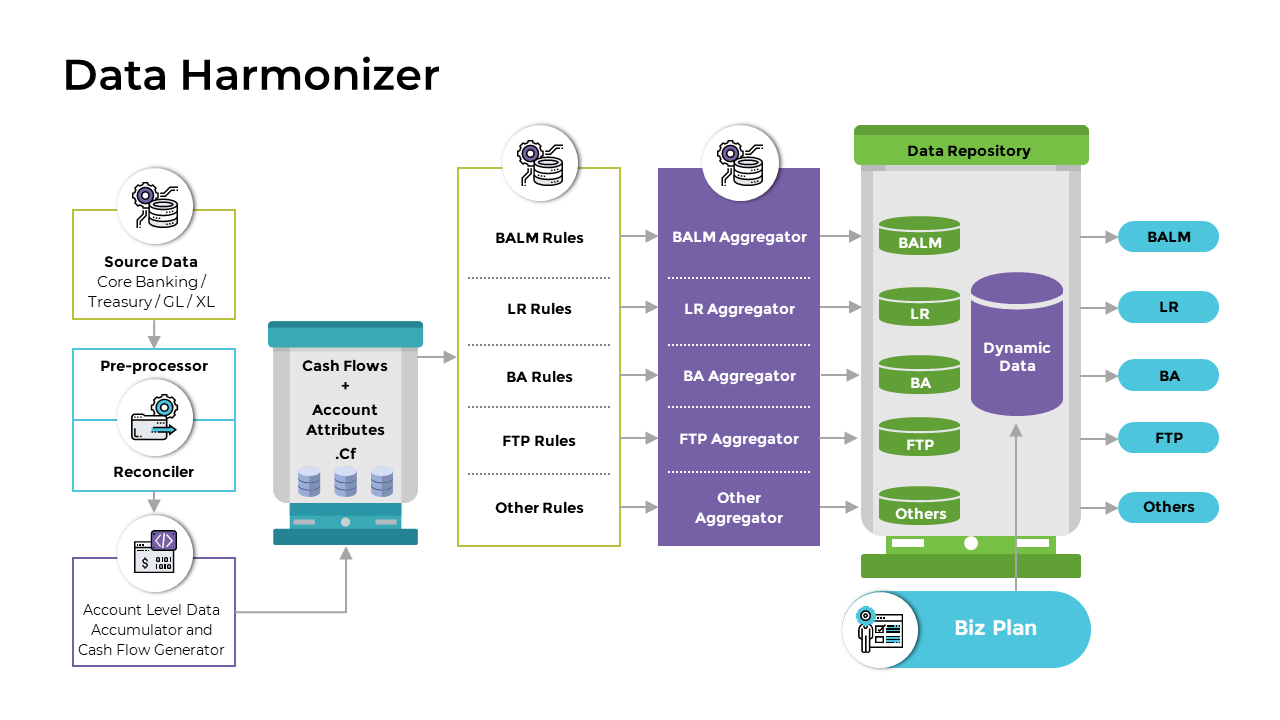

Surya was founded with a view to create products for financial risk management as understanding of risks, returns and capital deployed is very essential in any part of BFSI. Risk is measured on cash flows. It is important that one represents cash flow profiles of all financial holdings. This forms the basis of further risk measurements and management reporting. Surya’s products of computing future cash flows, deploy behavioural analysis to convert indeterminate maturity holdings to cash flows and harmonise all this data to enable multiple risks and financial analytics. Dynamism is introduced by way of scenarios for future business. Data is aggregated differently for different modules, and differently for MIS as well.

One set of analytical tools, which is very important in BFSI is Asset Liability Management. Broad pillars of ALM are structural liquidity risk, interest rate risk and balance sheet management. Liquidity module measures liquidity gap by timeframes, leading to the measurement of structural liquidity risk and lays basis for other measures such as Cost to Close, Maximum Cumulative outflow, Tolerance analysis etc. Likewise, functions in interest rate risk module such as repricing gap analysis, duration gap analysis and Sensitivity of NII, Market value of equity to interest rate movement are key measurements of interest rate risk.

More importantly, the movement of these analytics over timeframes defines the way an institution is trending on the risk-return equation. Monitoring of financial ratios, ability to have user-defined ratios, ad-hoc and scheduled ratio reporting, trend of ratios, trend of all variables, liquidity stress testing etc. help in balance sheet control and management. Surya’s solution for ALM is a true multi-currency, multi-scenario software.

With the adaptation of BASEL III liquidity frameworks, Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NSFR) has become a part of the regulatory process. Surya’s BASEL III LR module aggregates data from data harmoniser and supports this regulatory reporting. Further advances are being made to provide predictive LCR over a month in order to manage LCR.

Capital Adequacy measures are getting more and more complex. With increasing data sizes and increasing complexity, it is not feasible to calculate risk-weighted assets at gross level and in fact needs account level handling.

This is where data harmoniser comes into use as the same data used to aggregate for BALM can now be used to stamp Risk-Weighted Assets at account level. Credit, Market and Operational risk capital requirements are calculated. Capital allocation algorithms then allocate available capital as per rules specified and hence capital adequacy can be calculated and reported. Surya’s CARE reports and records capital adequacy requirements.

Funds Transfer Pricing module is a management accounting system, allocating a Funds transfer price to each position, enabling relative measurements. This will in turn yield branch profitability, customer profitability, RM profitability etc. This is a very important module to set the direction for a financial institution.

Income simulation is a very vital tool for BFSI. Both under static and dynamic scenarios, Surya’s IA simulate income at daily level, providing very accurate forecast of NII under multiple assumptions. Many product behavioural patterns are parameterised, providing a great degree of sophistication and accuracy. This is a great tool for financial control as business patterns can be driven by forecasts and forecasts can get more accurate.

IFRS9 Expected Credit Loss has become a universal standard of accounting in the domain of fair value accounting. Surya has a default probability of default and loss given default module. Besides, Surya’s IFRS9 offering can use PD and LGD from user’s systems and does not impose its own calculation methods on an institution. Data, however, comes from data harmoniser.

Interest Rate Risk on Banking Book (IRRBB) is an emerging regulation. Preliminary guidelines have been published and are being reviewed. Capital will have to be allocated for this risk as well. Surya has worked on this and is ready with the necessary solution.

To Summarise, regulators will demand lower level of granularity in reporting and support this, Surya has built its data harmoniser, which produces detailed data at account level were required to enable clean data provision for future regulations as well.

How is Surya assisting NBFCs in Asset Liability Management in adherence to the banking regulator?

Surya’ BALM being a very versatile ALM system, has been adapted to NBFC’s requirements. Reports of liquidity risk, interest rate risk, LCR are all required on a periodic basis. The day is not far off when NBFC’s will be treated on par with banks for regulatory reporting. Today, there is a differentiation between NBFC’s based on deposit-taking activity and the like.

Surya has always priced its products by module so that a customer need not pay for all modules regardless of usage. Thus, each NBFC is free to pick only those that are relevant to them.

Secondly, for smaller NBFC’s, a hosted model is available. Companies can upload their data, run Surya’s software in their instance for reporting. If this is tedious, Surya offers a run service where users may deposit data in a designated place and reports will be run by Surya and deposited back. Setups for all this takes time and effort.

Which technologies have you deployed for streamlining services for your clients?

Surya’s ALM has two distinct parts to it. The first is the Data Harmoniser and the second part is Analytics. Data Harmoniser which requires massive processing is hosted in Linux and written in Rust and does not need a database.

Surya supports Windows server, Rust and MS SQL Server as well for harmoniser. Analytics is database agnostic, supports SQL server, Oracle and PostGresQL and is written in Microsoft C#. Several advancements have been made in terms of multi-threading and multi-processing to get higher speeds. Data Harmoniser is achieved using completely open source technologies.

Big Ticket Lenders and NBFCs both are a part of your client list. Which one of these two is most dynamic to work with and why?

I do not believe there is a difference in dynamism based on these criteria. Some institutions are very dynamic and some are more conservative in terms of change. I believe there are enough examples of both categories on both big-ticket lenders and NBFCs. Regulatory push is one thing but internal management is more the reason why one should invest in this category of systems.

Elets The Banking and Finance Post Magazine has carved out a niche for itself in the crowded market with exclusive & unique content. Get in-depth insights on trend-setting innovations & transformation in the BFSI sector. Best offers for Print + Digital issues! Subscribe here➔ www.eletsonline.com/subscription/