Bringing the citizens under the umbrella of banking and digital financial services has remained a constant endeavour of our government and policymakers. Ambitious schemes such as the Demonetisation exercise, the Pradhan Mantri Jan Dhan Yojna (PMJDY), Digital India etc. are all part of this broader agenda of creating a cashless economy and extending the reach of digital financial services to the masses.

Bringing the citizens under the umbrella of banking and digital financial services has remained a constant endeavour of our government and policymakers. Ambitious schemes such as the Demonetisation exercise, the Pradhan Mantri Jan Dhan Yojna (PMJDY), Digital India etc. are all part of this broader agenda of creating a cashless economy and extending the reach of digital financial services to the masses.

Launched in August 2014, the PM Jan Dhan Yojna is aimed at achieving financial inclusion at the last mile. According to the PMJDY official website, as of August 15, 2018, there are more than 32 crore beneficiaries of the scheme. More than 24 crore RuPay debit cards have been issued to beneficiaries of these accounts so far. The Demonetisation move on November 8, 2016, was also launched with a larger goal to encourage people to opt for digital transactions and discourage them from making cash exchanges.

Launched in August 2014, the PM Jan Dhan Yojna is aimed at achieving financial inclusion at the last mile. According to the PMJDY official website, as of August 15, 2018, there are more than 32 crore beneficiaries of the scheme. More than 24 crore RuPay debit cards have been issued to beneficiaries of these accounts so far. The Demonetisation move on November 8, 2016, was also launched with a larger goal to encourage people to opt for digital transactions and discourage them from making cash exchanges.

However, despite such massive projects undertaken for financial and digital inclusion, at the ground level, a vast majority is still not using banking or fintech services, especially those at the base of the pyramid.

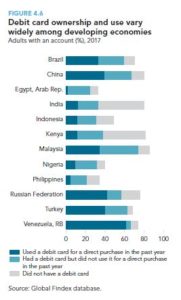

A World Bank report suggests that many JDY account holders might not have had an opportunity to use their bank accounts yet. According to the World Bank Global Findex Database for the year 2017, which measures financial inclusion and fintech revolution in a country, the share of inactive bank accounts among bank account holders is 48percent in India, which is the highest in the world and about twice the average of 25 percent varies across economies. “Part of the explanation might be India’s Jan Dhan Yojana scheme, developed by the government to increase account ownership,” the report says. Similar is the case of Debit card usage as per the report.

The Demonetisation efforts, even after more than 20 months, have not yielded much result as well. The dependence of the populace on cash continues to remain strong as ever. A November 2017 report by the Reserve Bank of India’s (RBI) Working Group on FinTech and Digital Banking stated that 40 percent of the population is currently not connected to banks and 87 percent of payments are still made in cash.

Given that our country has one of the fastest growing mobile, internet, and smartphone penetration, the reason for people not embracing digital channels for transactions, especially when it comes to availing financial services, may seem befuddling. The answer could lie in the skewed user base.

As per report jointly by Bain & Co, Google and Omidyar Network, of the 390 million internet users, ~80 percent (300 million) are from relatively affluent NCCS segment A, B, and C alone. A mere 13 percent internet penetration across lower-income NCCS D, E segments (just 90 million users in a base of 710 million) versus 73 percent across NCCS segment A.

Further, the transacting user base is small – of the 390 million users, only 40 percent (160 million) transact online which is skewed as well. 90 per cent transactors (40 million out of 160 million) from NCCS segments A, B, and C. As per the same report, top reason for non-transactors to not transact online comprise lack of trust, no touch and feel, convenience of offline, offline more reliable, no grievance redressal, cheaper offline and inability to find products

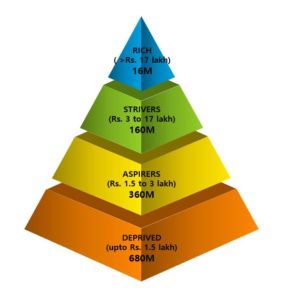

The above doesn’t seem surprising if we look at another report by JP Morgan, according to which Fintech companies in India have succeeded to cater to only 23 percent of the elite/affluent section of the Indian economy while a huge portion still remains untapped. The report says that rest of the 47 percent of the population, which comprises of people in the lower and middle-income growth, is a potential market and fintechs have a large opportunity to tap this market successfully.

Banks and fintechs have largely failed to think out of the box or even sometimes have neglected to serve the strata of the society, which is at the lower rungs of the economic pyramid.

Suvidhaa since its inception a decade ago has focused on serving the 1 billion people at bottom of pyramid and proven it can be a viable business proposition given the right product addressing the peculiarities of the segment, their needs and leveraging technology to build an effective and efficient service delivery model. Suvidhaa brought money transfer facility in the neighbourhood of millions of migrants in cities through its unique product-partnership-technology approach. It enabled small general merchants, neighbourhood kirana store with technology to serve their customers a wider bouquet of service and earn a better living. Suvidhaa brought India’s first digital finance product for customers at the base of pyramid. It is because of such a unique product /service offering, more than 40 million customers trust Suvidhaa.

Fintechs indeed have a sea of opportunity awaiting them considering the growing mobile and internet usage. The need of the hour is to think out of the box and introduce innovative solutions and services to effectively use digital channels in serving this segment which is still not digitally and financially included.

(The author of this article is Paresh Rajde, founder, Suvidhaa Infoserve Private Limited. Views expressed in this article are writer’s personal observation and doesn’t necessarily reflect The Banking & Finance Post’s point of view.)

Elets The Banking and Finance Post Magazine has carved out a niche for itself in the crowded market with exclusive & unique content. Get in-depth insights on trend-setting innovations & transformation in the BFSI sector. Best offers for Print + Digital issues! Subscribe here➔ www.eletsonline.com/subscription/