Joint Secretary, Financial Services, Government of India

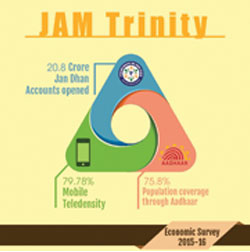

The trinity of JAM-Jan-Dhan Yojana, Aadhaar and Mobile-has the potential to revolutionise the Banking, Financial services and Insurance (BFSI) sector, provided there are some visionary officers, coupled with a strong political will, to take it forward, writes Rajesh Aggarwal, Joint Secretary, Ministry of Tribal Affairs, Government of India for Banking & Finance Post. Aggrawal is, however, apprehensive that this innovative idea could nipped in the bud by the wily file pushers in the government

JAM in governance would usually lead to a thought of how our bureaucracy has “jammed” the development by tying up all processes in red tape. Luckily, there are some in our bureaucracy who are not mere file pushers, and who can dream of new ideas. JAM is an idea which needs visionaries within the bureaucracy, which needs political inputs and constant  political oversight so that file pushers do not kill this idea. We need an army of start-ups who will disrupt existing systems, and these startups need to be insulated from old fashioned bureaucrats and regulators. And we need citizens who have seen the best-of-class services globally and will demand the same from our municipalities and government organisations.

political oversight so that file pushers do not kill this idea. We need an army of start-ups who will disrupt existing systems, and these startups need to be insulated from old fashioned bureaucrats and regulators. And we need citizens who have seen the best-of-class services globally and will demand the same from our municipalities and government organisations.

Let us start with “J” – the Jan Dhan, or more broadly the banking channels.

Five years ago, while working as Secretary (Accounts and Treasuries) in Maharashtra, I exhorted my Team to abolish cheque books used by Treasuries and DDOs (Drawing and Disbursing officers). They thought I had gone nuts, and said as much behind my back. Everybody knows that a clerk can hold on to a cheque due to an employee or a vendor (for some commission, speed money etc.), or even if nobody is demanding commissions, the citizen may have to make multiple trips (“sahib is on leave/has gone out for lunch/printer not working”). Hence, electronic transfer to the bank account of an employee, or a pensioner, or a kid getting scholarship, or to a vendor/contractor makes a lot of sense. Thus the idea of going cheque-less made so much common sense, and implementation was so easy, that vested interests could not stymie it, and we could go whole hog in six months. We kept it simple (“KISS – Keep it simple, stupid”). If software was not there, the DDOs and Treasuries were asked to give handwritten or typed “advice notes” to banks.

Now DBT is in fashion. What we did in Maharashtra five years ago, was classic, plain vanilla DBT (Direct Benefit/ Bank Transfer). We saw that going cashless and chequeless brought 30 per cent savings in some schemes! Ghost employees, pensioners and beneficiaries seem to vanish! Probably the bankers are afraid of ghosts, and don’t open their bank accounts! Or is it the other way around? Is it that even the ghosts are afraid of bankers?

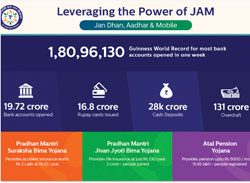

We know that common citizens are afraid of banks – the poor are afraid of even the guard standing on the door of the bank – stepping up inside the bank doors is something they could not even dream of. This is something that Jan Dhan program nailed very well. Though RBI (Reserve Bank of India) had floated simplified KYC norms for nofrill accounts, the poor would find it difficult to open bank accounts. The DBT thing cannot take off if poor people do not have bank accounts. Jan Dhan envisaged that every family in the country will have at least one bank account, and the bankers were told to go all-out to achieve this.

We know that common citizens are afraid of banks – the poor are afraid of even the guard standing on the door of the bank – stepping up inside the bank doors is something they could not even dream of. This is something that Jan Dhan program nailed very well. Though RBI (Reserve Bank of India) had floated simplified KYC norms for nofrill accounts, the poor would find it difficult to open bank accounts. The DBT thing cannot take off if poor people do not have bank accounts. Jan Dhan envisaged that every family in the country will have at least one bank account, and the bankers were told to go all-out to achieve this.

A masterstroke by the Prime Minister was to advocate zero balance account. Many analysts think that pull factors like added insurance cover, overdraft etc. are key factors behind the success of Jan Dhan – but I feel that zero balance account, along with free passbook and Rupay card are the key factors.

It is not about economy, stupid! This is more about Social Status rising. Thus, a villager without a bank account is poor, downtrodden, zero self-respect Parsu. When he opens zero balance account, he goes up in social status, and people call him Parsa bhai.

When he starts using bank, and proudly goes to ATM to withdraw money, he feels like and gets treated like Parasram ji. In Mission office, we get lots of feedback, and one particular letter I will always remember is the one which said – “Our village has a bank branch, but please give us an ATM, because the ATM does not insult us, or make us feel small” . Thus, in Jan Dhan Mission office, our team works more like passionate agents or catalysts of social change, rather than having the airs of working in an economic ministry.

Jan Dhan was never about bank account opening and DBT only.

A bit of Insurance (life and accident) and access to credit (overdraft) was inbuilt. This later evolved into market-priced, zero-subsidy insurance covers of Life and Accident (Pradhan Mantri Jeevan Jyoti and Suraksha Bima) schemes, at ridiculously low premiums. Beauty was that no fresh KYC was needed, auto-debit from bank account was done, subscription form was incredibly simple, and one could even subscribe by a simple SMS! No wonder, we sold more than 100 million subscriptions in two months! The easy-loan scheme of Mudra also evolved out of good feedback from Jan Dhan overdraft component. So many things can piggyride on a bank account!

We see new age in banking coming up. I love to talk to start-ups, to new FinTech guys. I have also been talking to new 11 payment bank teams. We have an opportunity to leapfrog, provided we don’t kill them with heavy regulation, with old-fashioned banker-style thinking. We need to totally redefine and reimagine – what is a bank, what is a branch, what is a passbook, what is a chequebook, what is KYC, what is a transaction. Traditional banking channels and software (RTGS, NEFT, remittances) are expensive and slow; telecom channels (mobile money, mPesa) are faster and less expensive; internet based channels (bitcoins or blockchain-based digital currency zipping over internet, undiminished in value) are much faster and almost have zero cost. Will we see the “WhatsApp” moment in banking, or will we let it go past us? The traditional incumbents will do every trick to kill the new-age players (“why should they get friendly eco-system and regulation when we got harassed so much?”). Thus the new airlines face roadblocks from existing players (recall 5/20), WhatsApp and Skype face roadblocks from existing Telecom players, new Payment banks will face many overt and covert challenges from existing players.

We see new age in banking coming up. I love to talk to start-ups, to new FinTech guys. I have also been talking to new 11 payment bank teams. We have an opportunity to leapfrog, provided we don’t kill them with heavy regulation, with old-fashioned banker-style thinking. We need to totally redefine and reimagine – what is a bank, what is a branch, what is a passbook, what is a chequebook, what is KYC, what is a transaction. Traditional banking channels and software (RTGS, NEFT, remittances) are expensive and slow; telecom channels (mobile money, mPesa) are faster and less expensive; internet based channels (bitcoins or blockchain-based digital currency zipping over internet, undiminished in value) are much faster and almost have zero cost. Will we see the “WhatsApp” moment in banking, or will we let it go past us? The traditional incumbents will do every trick to kill the new-age players (“why should they get friendly eco-system and regulation when we got harassed so much?”). Thus the new airlines face roadblocks from existing players (recall 5/20), WhatsApp and Skype face roadblocks from existing Telecom players, new Payment banks will face many overt and covert challenges from existing players.

I hope that new payment banks are not killed in the womb, by traditional treatment of KYC, Passbook, Chequebook, Branch concepts. Let us hope that banking regulator RBI will issue lightweight regulation for payment banks.

Jan Dhan was never about bank account opening and DBT only. A bit of Insurance and access to credit (overdraft) was inbuilt

Now, let us talk about “A” in JAM, which stands for Aadhaar.

There are many good things and bad things possible with Aadhaar- but being a government official, let me talk only about great, good possibilities with Aadhaar. First is obviously cleaning and de-duplicating any database – be it voter list, ration card list, driving license or passport, pensioners list, and so on.

Our databases – all of them – are in pathetic state, and linking with Aadhaar can bring some sanity, by removing duplicates, and by having uniformity of basic demographic and address metadata – making these databases “talk” to one another. (This unfortunately can lead to Big Brother watching the citizen at every step – in a democracy, it is essential that different departments remain isolated and don’t work in tandem to harass the citizen. Second benefit of centralised Aadhaar database is anytime, anywhere, online verifiable identity check (eKYC), working on open API methodology. This can let us leapfrog over many developed nations, provided we can change regulation accordingly.

Out Telcos may be wasting thousands of crores of rupees every year in collecting and preserving paper-based KYC documents. eKYC done at telecom franchises can result in instant SIM card activation and zero paperwork. Similarly, if a person does not want a chequebook, then banks don’t really need a wet signature, and the bank account opening process could be made paperless and eKYC based, saving the banks hundreds of crores of rupees every year, apart from being convenient for the citizen. Let us hope that the banking regulator RBI and telecom regulator TRAI will do something about this.

eKYC can help in proving you are you, and also that you are alive! Five years ago, as Secretary (Accounts and Treasuries) in Maharashtra, I would frequently chat with pensioners sitting in our Treasuries. The annual “main zinda hun” (I am alive) certificate by banker or tahsildar, can be painful to senior citizens. I vividly remember bouncing the idea to Nandan Nilekani, of eKYC machine giving “main zinda hun” certificate. Nandan, in his typical IIT lingo said “Boss, great idea!”. Now we see millions of pensioners linking their Aadhaar number to the pension databases.

Third, Aadhaar can be financial address, though at the moment, it is riding on top of a bank account. The first Aadhaar based advice note in the country was signed by me four years ago, as IT Secretary, Maharashtra. We worked with Bank of India and UIDAI, and gave an advice note of 50 BoI customers of Padga village in Thane district to the bank, with three columns – customer name, Aadhaar number instead of bank account number, and the amount (of 100 rupees each). The bank server resolved the Aadhaar number to the account number, pushed the money, and then gave the successful scroll to us. Next step was to make it work across banks. So we brought NPCI in, mixed customers of four banks, and gave this mixed list (with Aadhaar numbers instead of bank account numbers) to our bank. Our bank passed this list to NPCI, which resolved it between four banks, and so on. Now, we see more than 10 million Aadhaar-based financial transactions every month through NPCI!

Third, Aadhaar can be financial address, though at the moment, it is riding on top of a bank account. The first Aadhaar based advice note in the country was signed by me four years ago, as IT Secretary, Maharashtra. We worked with Bank of India and UIDAI, and gave an advice note of 50 BoI customers of Padga village in Thane district to the bank, with three columns – customer name, Aadhaar number instead of bank account number, and the amount (of 100 rupees each). The bank server resolved the Aadhaar number to the account number, pushed the money, and then gave the successful scroll to us. Next step was to make it work across banks. So we brought NPCI in, mixed customers of four banks, and gave this mixed list (with Aadhaar numbers instead of bank account numbers) to our bank. Our bank passed this list to NPCI, which resolved it between four banks, and so on. Now, we see more than 10 million Aadhaar-based financial transactions every month through NPCI!

Bank of India also experimented with embossing Aadhaar number on the front face of the debit card, and also embedding it in the magnetic strip. This had the added advantage that customer did not have to type in 12 digits into the POS/microATM. I hope that all banks will introduce this feature into credit/debit cards as well as mobile wallets, and also modify the software of ATM, microATM and POS machines to enable this.

WhatsApp, Facebook, and eCommerce have taught our citizens the value of mobile based transactions

Now, let us talk about “M” in JAM, which stands for Mobiles.

Almost every family in the country now has a bank account, aadhaar and mobile. The “M” in JAM should not be restricted to mobile banking, but should stand for use of mobiles in various eco-systems.

Mobile wallets (Paytm leading the pack), mobile banking apps, SMS-based money transfers, *99# based services available on feature phones in multiple languages etc. are gaining traction, but we all hope that the new payment banks and FinTech players will overturn many traditional concepts. Let us see how it evolves over next few quarters.

WhatsApp, Facebook, and eCommerce have taught our citizens the value of mobile based transactions. They now demand government services to be available in the same convenient, faceless fashion. After eCommerce, now health and education are the sectors witnessing disruption.

With 2G/3G/4G expansion, and with prices of Smartphones coming down (some say that Rs 4000 is the tipping point, which already has been achieved – forget about Rs 251 Ponzi!), we will see explosion of internet connected smartphones, and private sector as well as government organisations offering lot of stuff on mobiles! Interesting days are in sight! Let us JAM!

ABOUT THE AUTHOR

Rajesh Aggarwal, a B.Tech in Computer Science from IIT-Delhi (1983-87), joined IAS (Indian Administrative Service) in 1989. He has served in various positions in Maharashtra and Delhi. He has written a number of papers on eGovernance and handled large number of eGovernance projects. Read more at www.eGovernance.guru

Elets The Banking and Finance Post Magazine has carved out a niche for itself in the crowded market with exclusive & unique content. Get in-depth insights on trend-setting innovations & transformation in the BFSI sector. Best offers for Print + Digital issues! Subscribe here➔ www.eletsonline.com/subscription/