The Banking, Financial Services, and Insurance (BFSI) industry has long been at the forefront of technological innovation, embracing emerging technologies to drive operational efficiency, reduce costs, and deliver superior customer experiences. Over the past decade, the sector has harnessed the power of machine learning and data analytics to gain valuable insights, automate processes, and make data-driven decisions.

However, the recent breakthrough in generative Artificial Intelligence (AI) has ushered in a new era of disruption, redefining the boundaries of what is possible in the BFSI sector. Since the advent of large language models like ChatGPT in November 2022, the adoption of generative AI has accelerated rapidly, reshaping industries worldwide.

Transformative Impact of Generative AI on BFSI in 2024

1. Revolutionising Customer Interactions: Generative AI has transformed the way BFSI companies engage with customers, offering highly personalised experiences at scale. Bank of America’s AI assistant “Erica” has handled over 200 million client queries with a 95 per cent satisfaction rate, while HSBC’s “Amy” generates natural language summaries of reports and provides tailored investment advice to wealth management clients, processing over 3 million reports in Q1 2024 alone.

2. Automated Content Generation: Generative AI has disrupted operations through automated content creation for marketing, legal documents, reports, and more. JPMorgan’s COIN system saved $1.5 billion in legal costs by drafting 83 per cent of subsidiary disclosure materials in 2023, while insurance giants like AIG use Anthropic’s “Claude” system to generate thousands of tailored letters, policy documents, and communications, reducing turnaround times by 60 per cent.

3. Synthetic Data Revolution: Synthetic data created by generative AI models is a game- changer for training AI securely with limited data. Global banks like Citi and fintechs like Zest AI use generative models to produce unlimited synthetic data matching production distributions. Zest AI’s synthetic data modules helped a top 20 U.S. bank improve credit underwriting model accuracy by 24 per cent while ensuring compliance.

4. Trading and Investment Disruption: AI-powered quantitative trading strategies have gained significant traction, leveraging transformer models to extract signals from millions of data points and sources. Two Sigma’s “Cosmos” funds outperformed the S&P 500 by over 40 per cent in 2023, while hedge funds like Rebellion Research are going all-in on generative AI, with Augur driving 35 per cent outperformance.

5. Anti-Fraud and Risk Management Breakthroughs: HSBC’s “Ava” system leverages generative AI to scrutinize billions of transactions, communications, and documents, detecting money laundering with 65 per cent higher accuracy than rules-based systems. Large insurers like Prudential use generative transformer models from companies like CognitiveScale to read unstructured data sources and assess risks with up to 50 per cent higher accuracy.

6. Generative AI + Multimodal Interfaces: Combining generative AI with multimodal

voice/vision interfaces is creating seamless digital experiences. Capital One’s “Eno” system uses large language models and computer vision to let customers snap pictures of

documents to get information and advice, while Standard Chartered’s “Dot” allows clients to visually explore and get advice on financial products using voice commands.

Early adopters of AI in BFSI Projections for the Rest of 2024

Projections for the Rest of 2024

1. Hyper-personalisation in Wealth Management: Generative AI will enable a high degree of personalisation in wealth management services. AI models will analyse individual investor profiles, risk appetites, financial goals, and market data to generate tailored investment strategies and portfolios, leading to increased customer satisfaction and better investment outcomes.

Also Read | Gen AI X BFSI: Redefining the Future of Financial Success

2. Conversational AI as Primary Customer Interface: Advanced conversational AI assistants will become the primary interface for customer interactions across banking, insurance, and investment services. These AI-powered chatbots and voice assistants will be capable of understanding complex queries, providing personalised advice, and executing transactions seamlessly, available 24/7.

3. Fraud Detection and Prevention at Scale: Generative AI fraud detection systems will become highly sophisticated, capable of analysing massive volumes of data from multiple sources in real-time. By identifying even the slightest anomalies and patterns, these systems will help prevent financial crimes like money laundering, identity theft, and payment fraud on an unprecedented scale.

4. AI-Driven Trading and Portfolio Optimisation: AI-powered quantitative trading strategies will become mainstream, with generative models continually adapting to market conditions and generating trading signals based on vast datasets. Additionally, AI will be used for dynamic portfolio optimisation, rebalancing asset allocations based on changing risk factors and market conditions.

5. Integration with Blockchain and IoT: The convergence of generative AI with blockchain and Internet of Things (IoT) technologies will drive innovation in areas like secure data sharing, transparent supply chain finance, and real-time risk monitoring. Smart contracts on blockchain networks could leverage AI for automated execution based on predefined conditions.

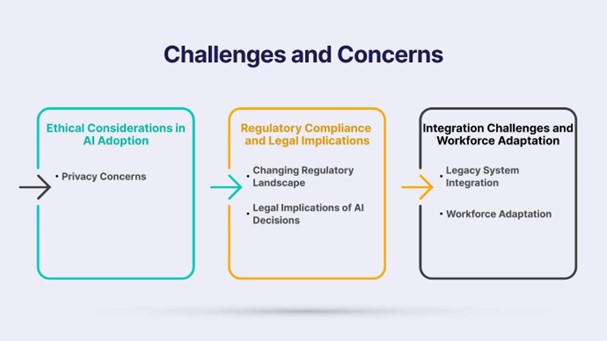

6. Responsible AI and Ethical Considerations: As generative AI becomes more pervasive, there will be an increasing focus on responsible AI practices, including data privacy, algorithmic bias mitigation, and ethical AI governance frameworks. Regulatory bodies will likely introduce guidelines to ensure AI systems in BFSI are transparent, explainable, and aligned with societal values.

7. AI Explainability and Bias Mitigation: One of the most pressing concerns within the BFSI sector regarding AI deployment is the lack of transparency and the potential for algorithmic bias. To address these issues, the industry is turning towards explainable AI (XAI) solutions. Leading technology companies such as Ericsson and Google, along with individual researchers, are at the forefront of developing AI systems that are not only powerful but also interpretable to users. Techniques like SHapley Additive exPlanations (SHAP) and Local Interpretable Model-agnostic Explanations (LIME) play a crucial role in this endeavor. These open-source methods, predominantly utilised by data scientists, enhance the transparency of AI decisions, making AI systems more understandable and trustworthy for financial experts and regulators. This move towards greater explainability is critical in building stakeholder trust and ensuring AI systems within BFSI adhere to ethical standards.

Impact on the Indian BFSI Sector

1. Government Initiatives and Regulatory Landscape: The Indian government’s initiatives like the Regulatory Sandbox and National AI Strategy will play a crucial role in shaping the adoption of generative AI in the Indian BFSI sector. The Reserve Bank of India (RBI) and other regulatory bodies will likely introduce guidelines and frameworks to govern the use of AI in financial services, ensuring data privacy, security, and ethical practices.

2. Fintech Collaborations and Partnerships: Indian BFSI companies will increasingly collaborate with fintech startups and AI solution providers to accelerate their AI adoption journey. These partnerships will bring together domain expertise, cutting-edge technology, and agile innovation practices, enabling faster development and deployment of AI-driven products and services.

3. Talent Development and Upskilling: To fully leverage the potential of generative AI, Indian BFSI companies will need to invest heavily in talent development and upskilling programs. This includes training existing employees on AI technologies, as well as attracting top AI talent from universities and research institutes. Interdisciplinary teams comprising domain experts, data scientists, and AI engineers will be crucial for successful AI implementations.

4. Use Cases in Rural and Underserved Areas: Generative AI will play a significant role in promoting financial inclusion in rural and underserved areas of India. AI-powered chatbots and virtual assistants will be able to communicate in regional languages, providing financial advice, product recommendations, and services to previously untapped segments of the population.

Also Read | The future of life insurance: AI, blockchain and tech-driven hyper-personalisation

5. Overcoming Data Quality and Infrastructure Challenges: One of the key challenges for Indian BFSI companies will be to overcome data quality issues and infrastructural limitations. Generative AI models require large, high-quality datasets for training, and companies will need to invest in data collection, cleansing, and management processes. Additionally, robust computing infrastructure and cloud capabilities will be essential for deploying and scaling AI solutions.

Why Must the Banking Sector Embrace the AI-First World?

In the rapidly evolving BFSI landscape, embracing an AI-first approach is no longer an option but a necessity. Generative AI offers a competitive advantage by enhancing operational efficiency, improving risk management, and delivering personalised, customer-centric experiences. Financial institutions that fail to adopt AI risk falling behind their more innovative counterparts.

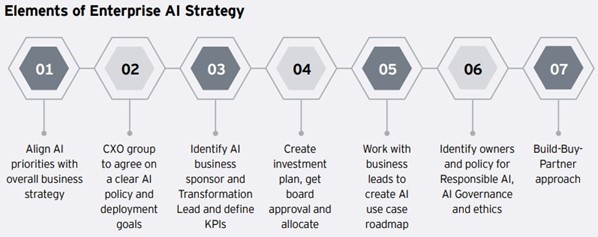

Recommended Enterprise AI Strategy – Steps to Become an AI-First Bank:

1. Develop an AI Strategy: Establish a clear AI strategy aligned with organisational goals, allocate resources, and foster a culture that embraces innovation and continuous learning. This strategy should be driven from the top, with strong leadership commitment and cross- functional collaboration.

2. Plan a Use Case-Driven Process: Identify high-impact use cases where AI can drive significant value, prioritise based on business needs, and develop a roadmap for implementation. This could include areas such as customer service, fraud detection, risk management, or personalised financial advisory.

2. Plan a Use Case-Driven Process: Identify high-impact use cases where AI can drive significant value, prioritise based on business needs, and develop a roadmap for implementation. This could include areas such as customer service, fraud detection, risk management, or personalised financial advisory.

3. Open Source Models vs. AI as a Service: Evaluate the trade-offs between leveraging open- source AI models or partnering with AI service providers, considering factors such as cost, customisation, and expertise. Open-source models may offer greater flexibility but require in-house expertise, while AI-as-a-Service providers offer ready-to-use solutions but may be more expensive.

4. Operate, Monitor, and Fine-tune Continuously: Implement robust monitoring and governance frameworks to ensure AI systems operate as intended, address any biases or issues, and continuously fine-tune models as data and requirements evolve. This includes establishing processes for model validation, explainability, and ethical AI oversight.

The generative AI revolution in the BFSI sector is well underway, unleashing a wave of transformation that will redefine how financial services are delivered and experienced. While the global BFSI sector has embraced this disruption, the Indian market is poised to catch up rapidly, driven by a thriving startup ecosystem, government initiatives, and the pressing need for innovation.

However, the adoption of generative AI is not without its challenges, and financial institutions must address concerns around data privacy, ethical AI governance, and workforce skill development. By striking the right balance between innovation and responsible deployment of AI, the Indian BFSI sector can unlock unprecedented opportunities, fostering financial inclusion, enhancing customer experiences, and driving sustainable growth in the digital age.

Views expressed by Chandramouli Pandya, Chief Technology Officer, Humane Technologies

Elets The Banking and Finance Post Magazine has carved out a niche for itself in the crowded market with exclusive & unique content. Get in-depth insights on trend-setting innovations & transformation in the BFSI sector. Best offers for Print + Digital issues! Subscribe here➔ www.eletsonline.com/subscription/